04/2026 We had a Gold Problem

| Date: March 2026 | Commit: ca71243 |

A system designed to respond to "stress" in the markets can also over-respond to it. This was one of the central problems to address in last month's refactoring.

When multiple independent macro signals all fire simultaneously the way they did in a genuine situation of crisis (oil shock, new war in the Middle East), their combined weight adjustments can push a portfolio to an extreme that no single signal was designed to produce.

The Problem: Signal Stacking

Our Stability Core operates on a series of macro signals that shift the portfolio away from its base allocation when stress conditions are detected. In a severe macro deterioration, multiple Tier-1 signals can fired at once, shifting bonds for example:

yield_curve_deeply_inverted: +0.15 shift to bondscredit_stress_severe: +0.10 shift to bondsglobal_inversion: +0.10 shift to bonds

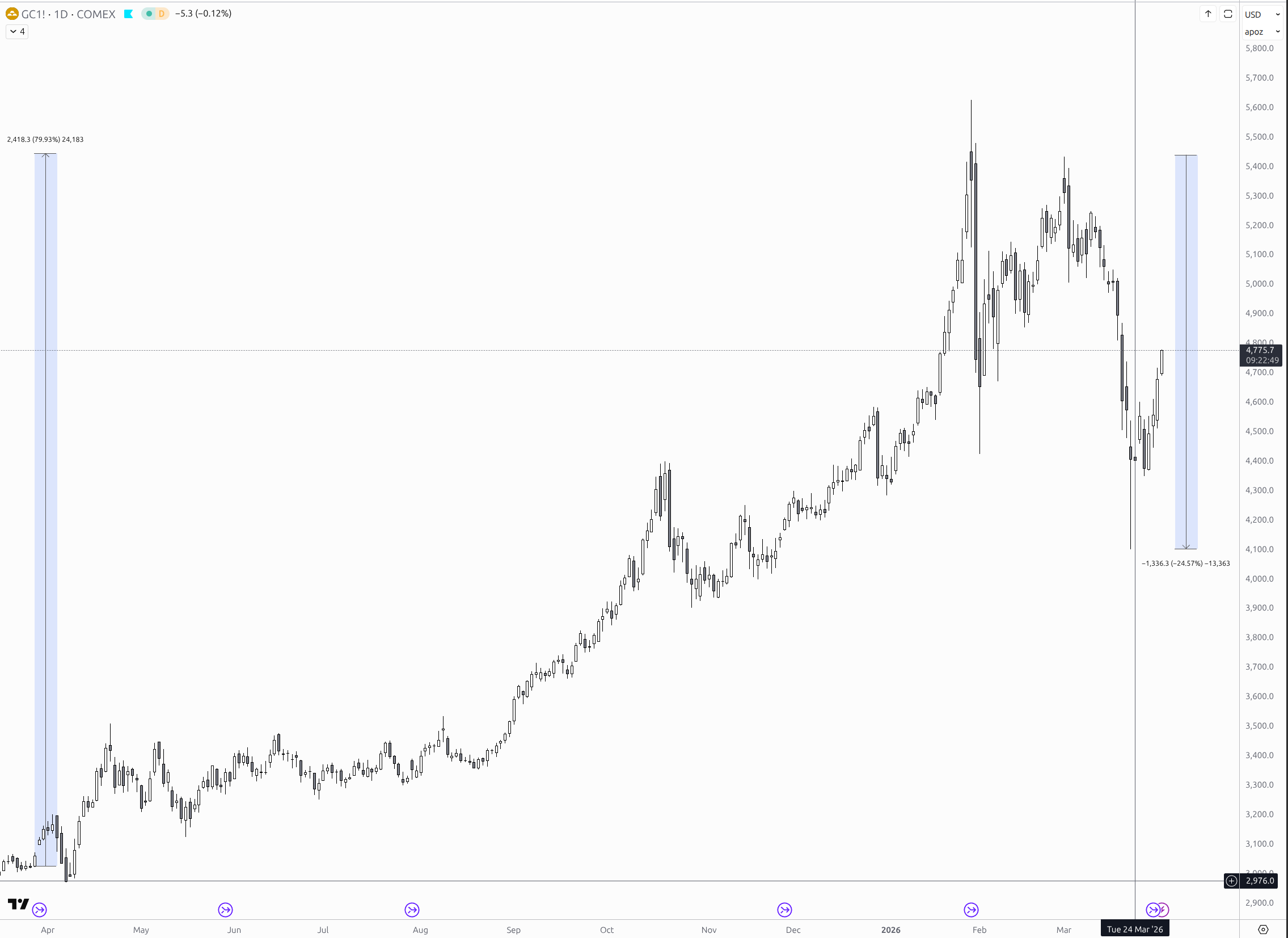

The result was a combined +0.35 added to a 20% bonds base, so a 55% total bonds allocation in a single rebalance cycle. Simultaneously, and in the case of this month more severely, gold received shifts from multiple signals, pushing from 7.5% base to 22.5%.

This was intended to act as a safety net for a "panic" month, but did not take into account the specifics of an oil shock, dollar strengthening regime, in which (an overbought) Gold took a SERIOUS hit:

After these shifts, the equity allocation was nearly dismantled. The portfolio is holding 55% bonds, 22.5% gold, the rest in commodities. (Bitcoin got removed after breaching momentum filters.) This was not the cautious portfolio I intended to come out as a result.

Since it was not produced by any deliberate design decision, I opted to pause the portfolio in March to work on integrating mechanisms for the current regime, backtest them and resume with an updated application.

As we need to keep in mind not to curve-fit to the 2026 scenario, I kept the approaches generic enough and leaned on documented and well researched concepts.

Per-Asset Shift Caps

A first blunt but effective path is to fix the maximum cumulative shifts above the base allocation that any asset can receive. These caps are applied after all signals are computed and their individual shifts are summed. This way, the portfolio still receives a meaningful defensive tilt without abandoning its equity exposure entirely.

Regime Preservation

The key idea here is for the caps to preserve the direction of the signal, but limit the magnitude. If all signals say "be more defensive," the portfolio should be more defensive, but not break the structural integrity of the portfolio.

Inspired by: the US Federal Reserve's "measured pace" guidance. Signal the direction of travel clearly while constraining the speed of movement to what the system can absorb.

Signal Independence Is an Illusion

The yield curve, credit spreads, and VIX are often treated as independent signals in academic papers, but are not independent in a crisis. The correlation between these three indicators approaches 1.0 during periods of actual financial stress because they are all measuring different aspects of the same regime shift: risk aversion spiking and liquidity withdrawing at the same time.

This is what made the 2008 financial crisis so severe: a series of individually observable early-warning signals (inverted yield curve in 2006-2007, rising credit spreads in early 2008, VIX spike in September 2008) deceivingly looked like independent data points until too late.

For our signal-based portfolio, this means we cannot simply sum signals as if they were independent. If Signal A and Signal B both fire because of the same underlying condition C, applying both shifts is effectively double-counting condition C's influence. The shift cap is a practical (even if somewhat blunt) safeguard against this.