The 2026 Refactor

It was time to rebuild from scratch. I reworked our allocation engine into two dedicated books, that each follow different goals.

Overlapping with the US-Iran military conflict, I went into a refactoring period for my previous allocation engine with the goal to isolate the individual sub-portfolios (books) more strictly. Too often did the KPIs for each of them get mixed up and entangled, while they actually need to be measured differently.

A Clean Split

The literature on portfolio construction tends to conflate two different questions:

- what should the portfolio look like?

- where do its returns come from?

Treating these as one question is how you end up with "alpha or it didn't happen" as the implicit verdict on everything. To avoid this, I reworked our allocation engine into two dedicated books, that each follow different goals.

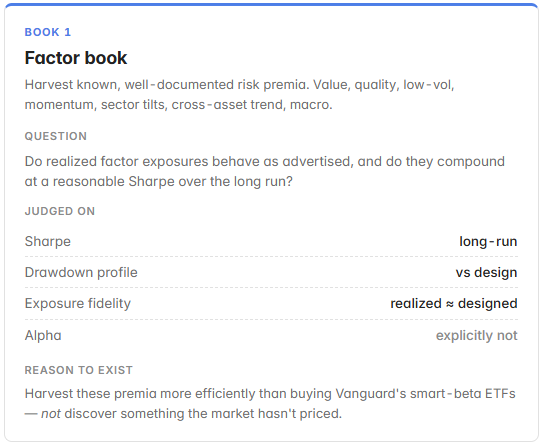

(1) The Factor Book

Capital allocated to "sleeves", whose job is to harvest known, well-documented risk premia: Value, Quality, Low-Volatility, Momentum, Sector Tilts and Macro Factors.

The strategies in this book are *not* judged on whether they produce alpha. They're judged on Sharpe, Drawdown Profile, and the extent to which realized factor exposures match designed factor exposures. The reason for existing is "harvest these premia more efficiently than buying Vanguard's smart-beta ETFs," not "discover something the market hasn't priced."

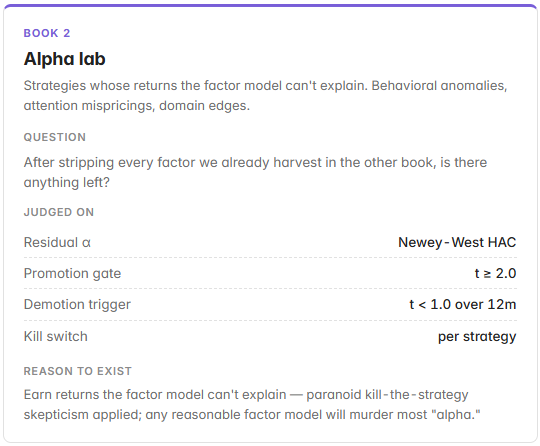

(2) The Alpha Book

Capital allocated to strategies whose returns aren't explained by the factor models. Behavioral anomalies, attention-based mispricings, domain-specific edges. These *are* judged on residual alpha, with a significance bar (HAC t ≥ 2 for promotion, < 1 over a rolling 12 months for demotion). Selection here is not merely automated, but the engine delivers tools, templates and daily screenings to help fundamental analysis and discretionary decision making.

I will also (partially) structure these differently using options combinations to target to capture catalyst effects on pre-defined risk and timelines.

These two books are mechanically independent. Trying to deliver on both at once with one verdict framework (which is what V1 did ) leads to complications and unexplained gains that we can not cleanly attribute to our engine's work.

Two Sigma's Venn platform makes this decomposition explicit: portfolio returns decompose into macro factor contribution, style factor contribution, and a residual Alpha.

The portable-alpha literature (Russell, BlackRock) similarly treats the factor engine and the alpha engine as separable layers that can be combined via derivatives or separate capital.

Our new model is closer to Portable Alpha in spirit but separates the two books.

What about "a bit of both"?

Time-series momentum is the obvious example. Moskowitz, Ooi and Pedersen (2012) show diversified time-series momentum across asset classes delivers substantial abnormal returns with little exposure to standard asset-pricing factors.

So, is this alpha or factor?

For our purposes: factor. The literature on the trend premium is robust enough across markets and decades that it earns a slot in the "known risk premium" bucket. The trend sleeve goes in the factor book and we can decide / review if it actually delivers in the next years.

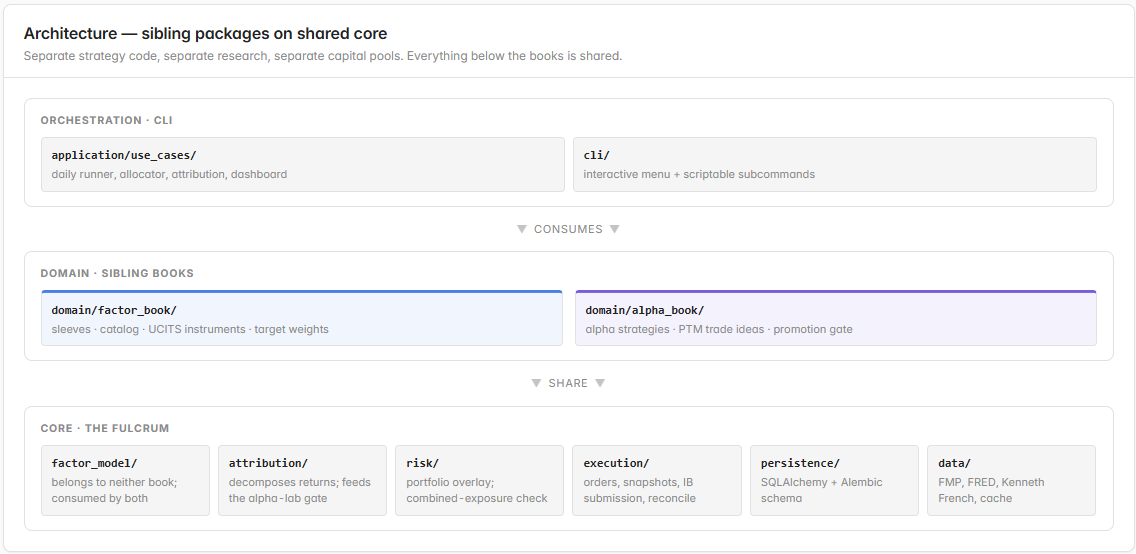

What this implies for the architecture

Three things, all flowing from the separation:

- Separate Factor sleeve code is systematic, parameter-driven, calendar-rebalanced. Alpha strategies are heterogeneous, sometimes event-triggered, sometimes opportunistic.

- Separate Research streams allow Alpha research to follow paranoid kill-the-strategy skepticism and Factor research to be transparent and parameter-driven

- Separate Capital Pools will allow each book to get its own capital allocation and its own kill switch. The factor book most likely runs at ~80%weight to start (the strategies have evidence; new alpha is speculative until proven). The portfolio overlay sits above both and checks that the combined factor exposures don't breach risk limits.

- Shared infrastructure like Data layer, factor model, attribution engine, execution layer and persistence .

Sources

Two Sigma, *Venn Factor-Based Risk Analysis*, factor analytics documentation. The decomposition into macro + style + residual is the standard institutional attribution pattern; the alpha lab's promotion gate is just this decomposition with a significance bar.

Russell Investments, *Portable Alpha: A Primer* (white paper); BlackRock Investment Institute, *Alpha and Beta Separation* notes. Both describe the same architectural move: factor exposures as a "beta engine" with residual alpha layered on top, optionally via derivatives.

Moskowitz, Ooi and Pedersen, "Time series momentum," *Journal of Financial Economics* 104 (2012), 228–250.

The pattern that anomaly returns concentrate in low-media- coverage firms is broadly documented; recent work building on Hong, Lim and Stein, "Bad news travels slowly: size, analyst coverage, and the profitability of momentum strategies," *Journal of Finance* 55 (2000), 265–295.

For idiosyncratic-momentum work, see Blitz, Hanauer and Vidojevic, "The idiosyncratic momentum anomaly," various 2018–2020 working papers; the effect survives newer factor models including q-factor and Stambaugh-Yuan variants.