The Factor Book

What factor investing actually is

Most investors are taught to ask which securities should I own? Factor investing asks a different question: which characteristics do I want to be exposed to? A factor is a measurable, persistent trait of a security, like how cheap it is relative to selected fundamentals, how strongly it has trended (momentum measure), how profitable the underlying business is and so on. These help explain why one group of assets earns a different return, at a different risk, than another.

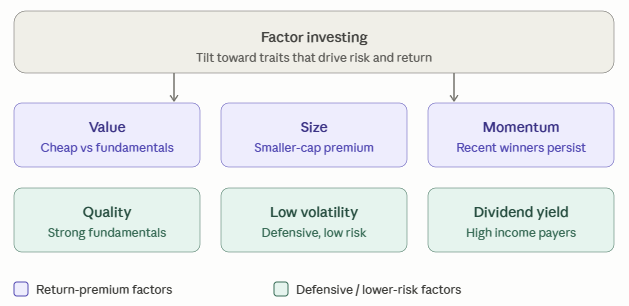

The concept has been established over five decades of research and a handful of traits have been isolated that have historically earned a return premium. (= A reward for bearing a particular risk.) While the way to measure each of them can still vary, the "buckets" many practitioners landed on are Value, Size, Momentum, Quality, and Low volatility. (Dividend yield for some portfolios.)

Once cleanly defined, they stand for deliberate sets of exposures, each of which we can dial up or down.

Why we're building this

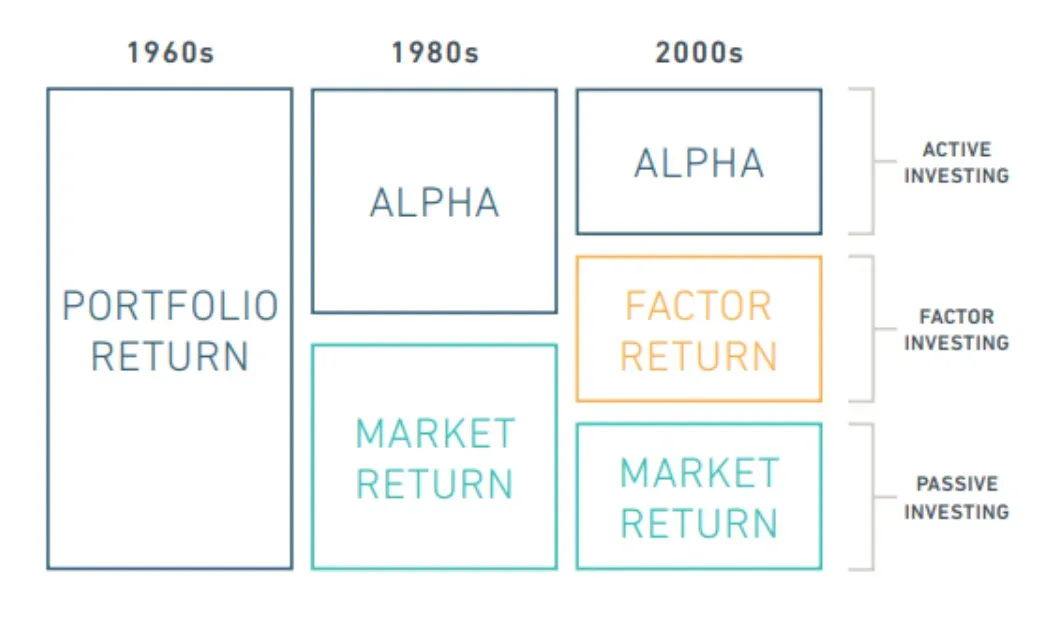

The factor book will be our guide of where our return and risk will actually come from. It will be the backbone of our systematic, multi-strategy portfolio. Every "sleeve" (=sub-portfolio with a dedicated goal) we run is a dedicated factor bet.

Writing the rules of this book down imposes honesty by forcing us to separate the return we get cheaply from (a) broad market exposure (US500 to begin with), the return we get from (b) factors, and the return from (c) fundamental, discretionary selection. This helps us avoiding to pay an "alpha fee" for something a rules-based tilt delivers at a fraction of the cost.

No single new "fourth stream" has replaced the (a) Market / (b) Factor / (c) Alpha combination as the dominant conceptual framework over the last two decades, but it has been refined and extended.

The important refinements are

(1) A formal split of "factor" into macro factors (growth, inflation, real rates, credit, liquidity, emerging markets) versus style factors. (Value, Momentum, Quality, etc.)

(2) Breaking down hundreds of documented factors into a smaller set of ~13 "themes". (Jensen-Kelly-Pedersen)

(3) The rise of AI asset-pricing models that treat alpha, factors and market as joint outputs of a stochastic discount factor.

The same evolution seen in the chart above is the basis for MSCI's July 2025 retrospective, Factor Indexing Through the Decades, which puts more than USD 6 trillion in factor-based mandates across active, indexed, and ETF vehicles today.

Refinement 1: Factor splits into macro and style

BlackRock frames two types of factors: macroeconomic factors, which capture broad risks shared across asset classes, and style factors, which explain differences in return within an asset class. Its Market Advantage framework names six macro factors — economic growth, credit, emerging markets, liquidity, real rates, and inflation — and treats the familiar style factors (value, momentum, quality, low volatility, and so on) as a separate layer sitting beneath them. MSCI's multi-asset-class model uses the same logic, arranging drivers in a pyramid from macro factors at the top down to security-level characteristics at the base.

The practical effect is to turn the three-stream model into a four-layer one: market return, then macro-factor returns across assets, then style-factor returns within assets, then whatever idiosyncratic alpha remains.

Refinement 2: Down to a handful of themes

By the early 2010s the literature had produced so many candidate factors that John Cochrane described a "zoo of new factors."

Harvey, Liu and Zhu (2016, Review of Financial Studies) catalogued 316 factors across 313 papers and argued that the threshold for a credible discovery should rise from the conventional t-statistic of roughly 2.0 to about 3.0. Hou, Xue and Zhang's Replicating Anomalies found that a large share of documented effects simply did not hold up, so the vast amount of factors were the product of data mining, not real premia.

The most important aggregation was done by Jensen, Kelly and Pedersen (2023, Journal of Finance): the majority of asset-pricing factors cluster naturally into 13 themes and their public dataset is becoming a de facto organizing scheme. (see also practitioners work like Swade, Hanauer, Lohre and Blitz, Journal of Portfolio Management, 2024)

Refinement 3: Machine learning and AI

The third refinement is the "newest frontier", and it is likely going to shape the framework over the next decade.

Machine-learning asset pricing tends to embrace the previously reduced huge number of factors. Rather than using a handful of specified factors, these models estimate the stochastic discount factor directly from hundreds of characteristics. Gu, Kelly and Xiu (2020) showed that neural networks and tree models substantially outperform linear benchmarks out-of-sample.

This is why the industry's vocabulary is slowly changing from "factor investing" to "systematic investing." When Invesco renamed its flagship survey in 2023, it was highlighting their new toolkit now includes macro and regime signals, alternative data, and AI.

What this means in practice

Even with all the new tools in AI and machine learning growing in importance, he language at the major managers has not changed. BlackRock, AQR, MSCI, Invesco, and Robeco still describe returns as some combination of market return (beta), factor or style premium, and discretionary alpha.

However, a great deal of what was once sold as alpha is now available as cheap, replicable factor exposure, so called "smart beta." As a result, portfolios now sit on a whole spectrum running from cheapest to most expensive: traditional market-cap beta, strategic or "smart beta" (long-only factor tilts), "alternative risk premia" or "exotic beta" (long-short, multi-asset, market-neutral, once claimed by hedge-fund alpha), and finally pure alpha.